Monthly QIS Review - September 2025

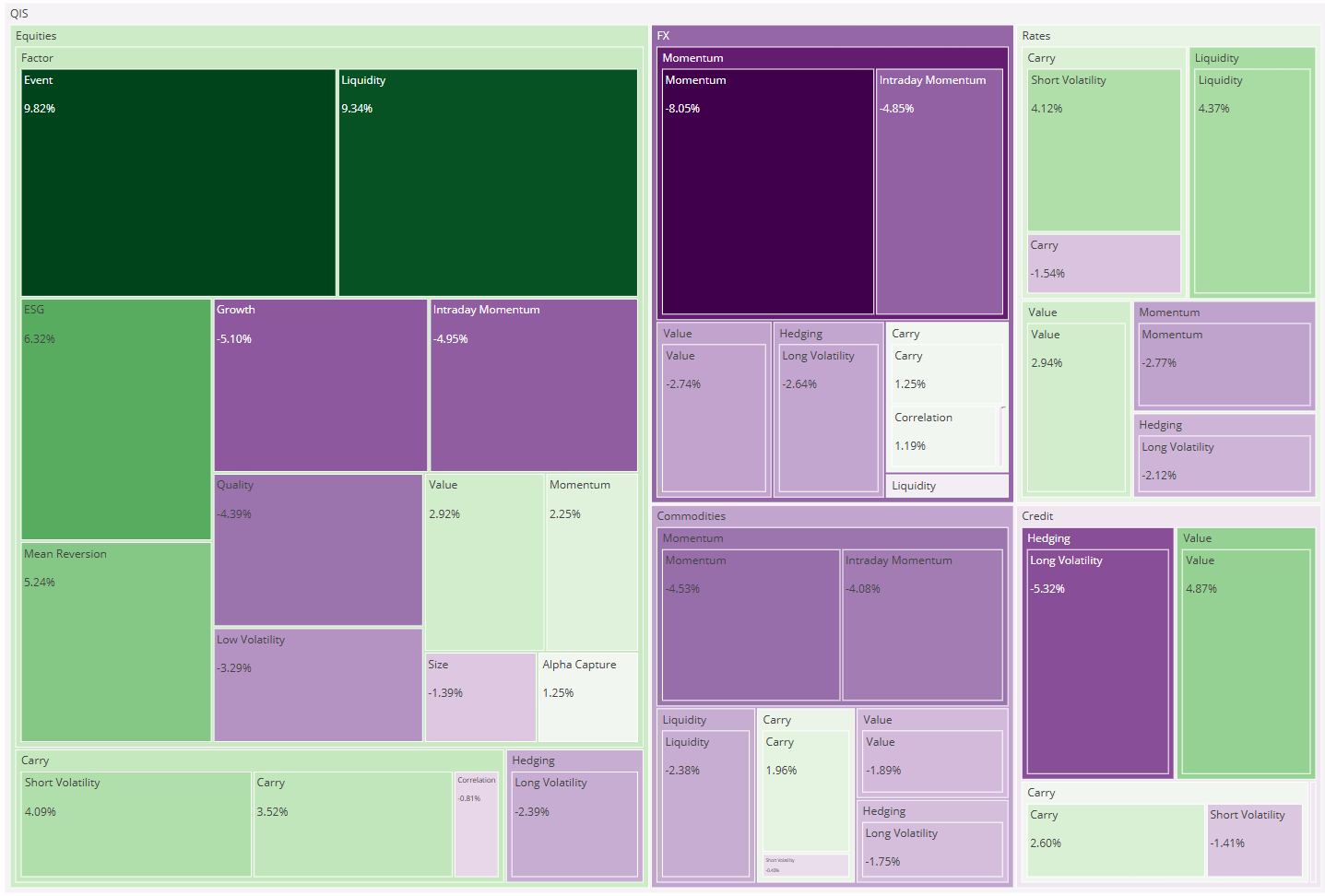

Executive Summary September 2025 was mixed but modestly positive for quantitative‑investment strategies (QIS). The average composite returned +0.26% MTD, with 20 of 42 strategies (≈48%) finishing higher. Cross‑sectional dispersion widened ...

4 min read