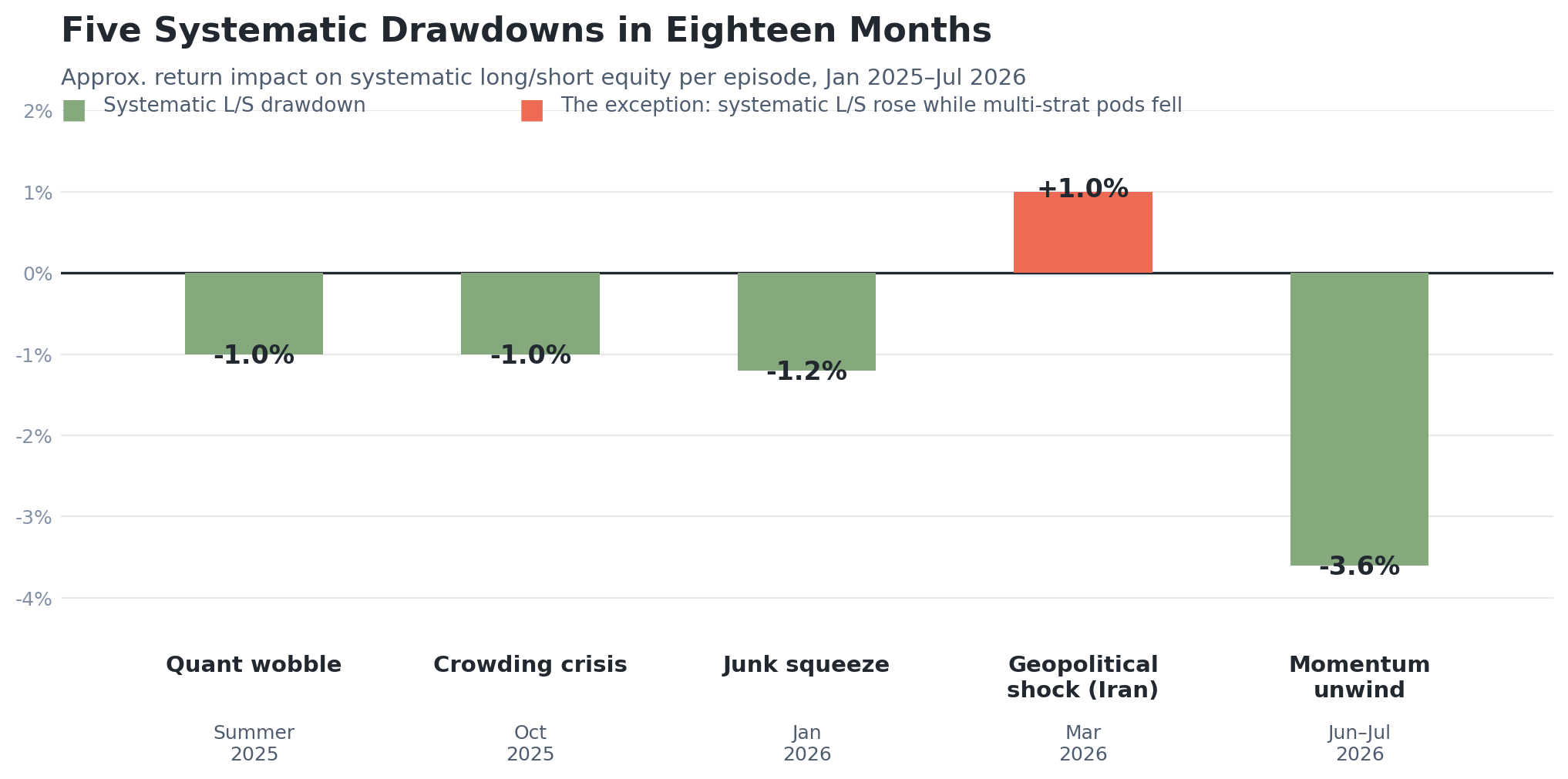

Eighteen months, five drawdowns, one mechanism — and one week in March that didn't follow the pattern.

6 min read | Jul 13, 2026

It's the first week of July, and the book is still working through the sharpest momentum unwind since 2023 — two weeks of losses that gave back roughly a quarter of the year's gains, per Goldman's prime brokerage desk. It's the fifth time in eighteen months a systematic drawdown has forced everyone to relearn the same lesson. Sitting here now, the pattern is easier to see than it was living through any one of them.

The four that rhyme

Run a book through eighteen months of this and you stop treating each episode as a one-off. They start to rhyme.

Summer 2025 first: public reporting on the "quant wobble" — which MSCI's research attributed to unusual factor correlations across value, momentum, and quality — named Two Sigma, Man Group, and Renaissance among the funds affected. Then October: systematic funds reportedly lost money in a month when equity markets hit new highs; the models had the direction right, the AI rally ran exactly as the signal said it would, and the book still bled, because the position couldn't be trimmed without moving the tape against itself. January brought a squeeze in lower-quality "junk" names that punished short books specifically — the kind of week where the short book does all the damage and the P&L attribution makes it obvious within hours. And now this: the momentum unwind through late June and into July, driven by AI, memory, and Korean equities, the worst two-week stretch for the strategy since 2023.

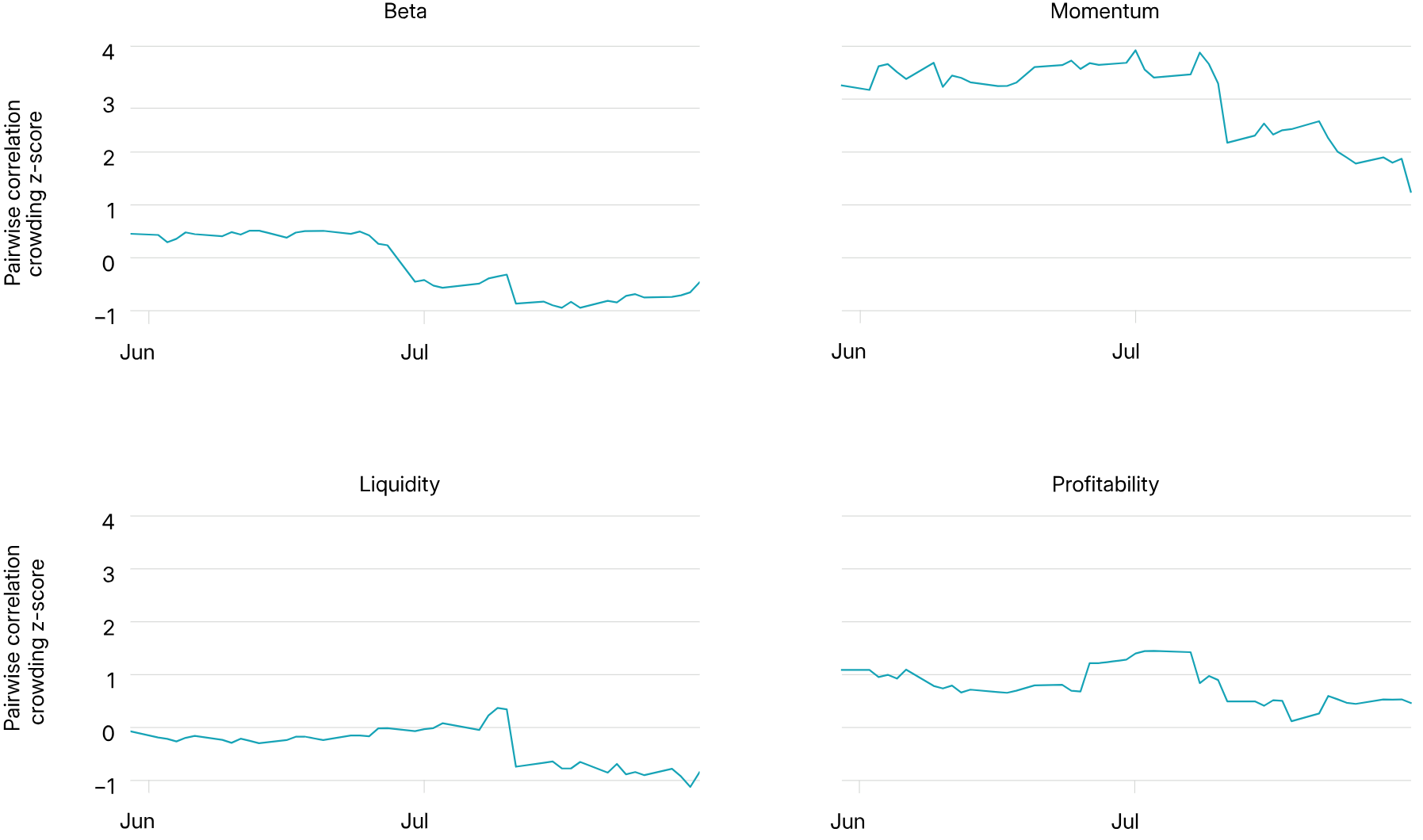

Signs of a crowding unwind for four of the key factors driving markets in the quant wobble

Source: MSCI Research; The pairwise correlation score in the MSCI Integrated Factor Crowding Model measures the average specific return correlation of stocks in the top and bottom quintiles of a factor over the trailing 63 trading days

Four episodes, four different triggers, one mechanism each time: a crowd builds, volatility rises, deleveraging stops being a decision and becomes a rule firing, and everyone heads for the same door at once. None of that is a new idea — we wrote about the momentum-specific version of it back in May. What's become clear only with eighteen months of hindsight is how often the door has been getting used, and how little the trigger seems to matter once it does.

Source: Resonanz Capital, based on data reported by Goldman Sachs, Reuters, Bloomberg, and MSCI Research

The one that doesn't.

Then there's March — and looking back on it now, it's the month that actually complicates the story, not confirms it.

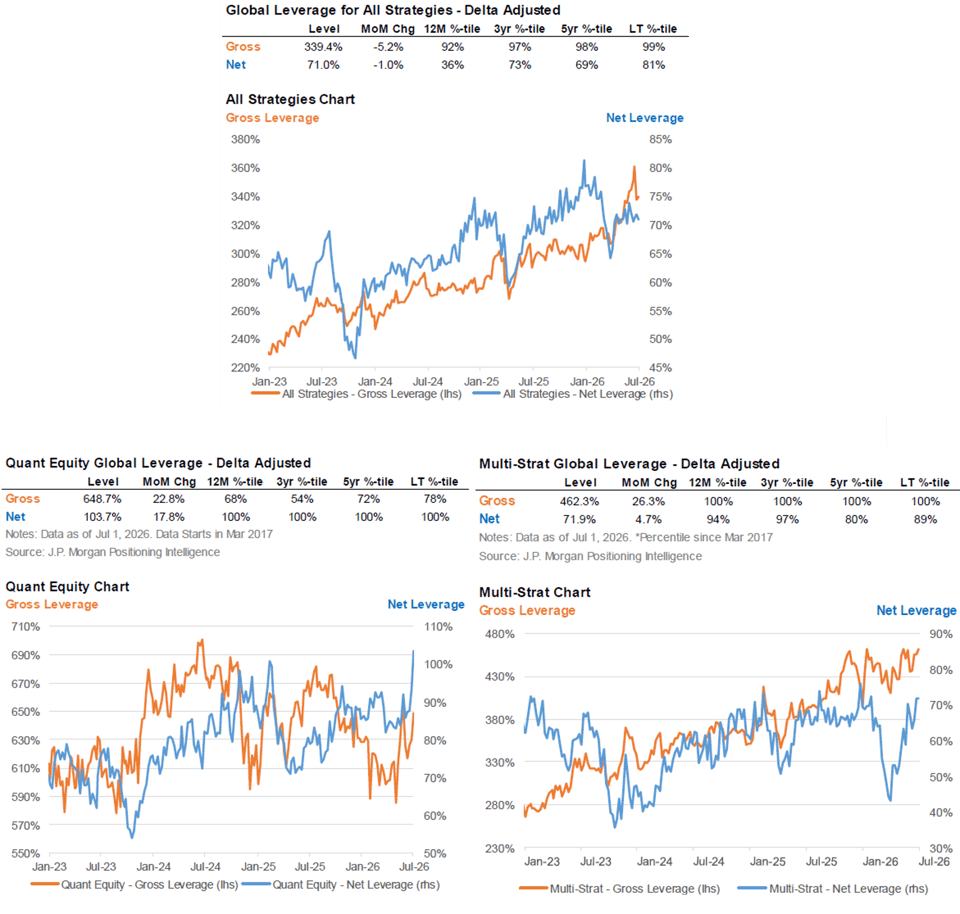

Systematic long-short equity rose by roughly one percent that month, according to prime brokerage data reported by Reuters and Goldman Sachs. In the same week, several of the largest multi-strategy platforms lost billions of dollars. Industry reporting put Millennium's and Point72's losses at roughly $1.5 billion each, Citadel's near $1 billion, and Balyasny's approaching the same figure — concentrated heavily in fixed income and macro books. The trigger was geopolitical, not a factor reversal: the shock associated with the Iran conflict, landing on a market already carrying near-record hedge fund leverage, with multi-strategy and quant books running at 444% and 645% gross respectively, according to prime brokerage data reported by Reuters. Millennium, Citadel, Point72, and Balyasny aren't quant shops — they're multi-strategy platforms, running a mix of systematic and discretionary books across hundreds of independent pods. What connects them to a pure systematic momentum unwind three months later isn't a shared label. It's a shared mechanism: leverage and crowding built up in one corner of the book, and when the shock hit, deleveraging happened all at once, the same way it did for the quants in July — regardless of whether a human or a model was pulling the trigger on any single position.

Hedge Fund Leverage Rising

Source: JP Morgan

The platforms in question sell diversification as something the model itself produces: dozens or hundreds of independent pods, centralised risk management, low correlation to any one factor. That's the pitch every allocator has heard, and most of the time it holds. March was the week it didn't. When several large platforms are carrying overlapping rates and macro exposure at the same moment, and a shock forces simultaneous de-risking across all of them, the independence stops being real — not because anyone broke a rule, but because a dozen pods that looked uncorrelated on a factor sheet were all quietly leaning on the same regime. You don't see that in the risk report until the regime moves.

Systematic long-short equity wasn't standing in that crowd in March. Three months later, it found its own — a completely different factor, for a completely different reason.

What eighteen months actually taught

The easy read, sitting here after five episodes, is that systematic strategies are simply getting more fragile. That's the wrong lesson, because it treats "systematic" as one risk with one failure mode. March said otherwise. A momentum book and a macro/rates pod can both be running fully systematic processes and still be standing in completely different crowds, exposed to completely different triggers, with completely different outcomes in the same month.

What that means in practice, if you're the one sizing the book: the question was never "are we systematic" or even "are we crowded." Every systematic strategy is crowded somewhere — that's what it means for a signal to have scaled. The question that actually matters is narrower and less comfortable: which specific factor is the crowd built around right now, what does this book's exposure to that specific factor actually look like once you strip out the netting, and what's the rule — a VaR limit, a vol target, a margin call — that would force this book to cut risk at the same moment as everyone else running the same trade. You don't answer that by predicting the next shock. You answer it by knowing, before the shock arrives, which crowd you're actually standing in — because the label tells you almost nothing about that, and the P&L will tell you too late.

None of the five episodes above happened because anyone's process was broken. They happened because a lot of capital was pointed at the same trade, under the same constraints, at the same moment — and being right about the signal didn't matter once the exit became mechanical. Eighteen months in, the book that survives the next one won't be the book with the best signal. It'll be the one that knew, ahead of time, exactly which door it was standing near.

Conclusion

Eighteen months of this doesn't add up to a checklist. It adds up to one discipline: stop asking whether a book is systematic, and start asking which crowd it's standing in today. Five episodes said the same thing five different ways. The sixth is already building somewhere, in some factor nobody's watching yet — and the only real edge left is noticing before the door gets crowded, not explaining afterward why it was.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.