June's tape withdrew two risk premia at once — and rewarded the strategies that harvest a repricing without being caught in one. Here's what the data said, and what it sets up for July.

5 min read | Jul 3, 2026

June was a modest month on average but a cleanly split one underneath, and the reason was that two of the year's supporting premia were pulled away in the same four weeks.

The Middle East war premium that had carried energy and gold through the spring unwound as a ceasefire framework took hold: the Strait of Hormuz reopened, Brent fell roughly 30% from its late-May peak, and gold slid to a seven-month low. At the same time, a Fed under new leadership swapped its rate-cut bias for a signal that the next move could be a hike — holding at 3.50%–3.75% but flagging tightening, lifting the dollar to its best month in nearly a year and sending the 10-year on an intramonth round-trip toward 4.38% and back to ~4.44%.

That is a very specific environment: premia monetize cleanly where markets reprice but do not break, and trend and convexity struggle where the defining moves are violent reversals rather than durable trends. June delivered both halves.

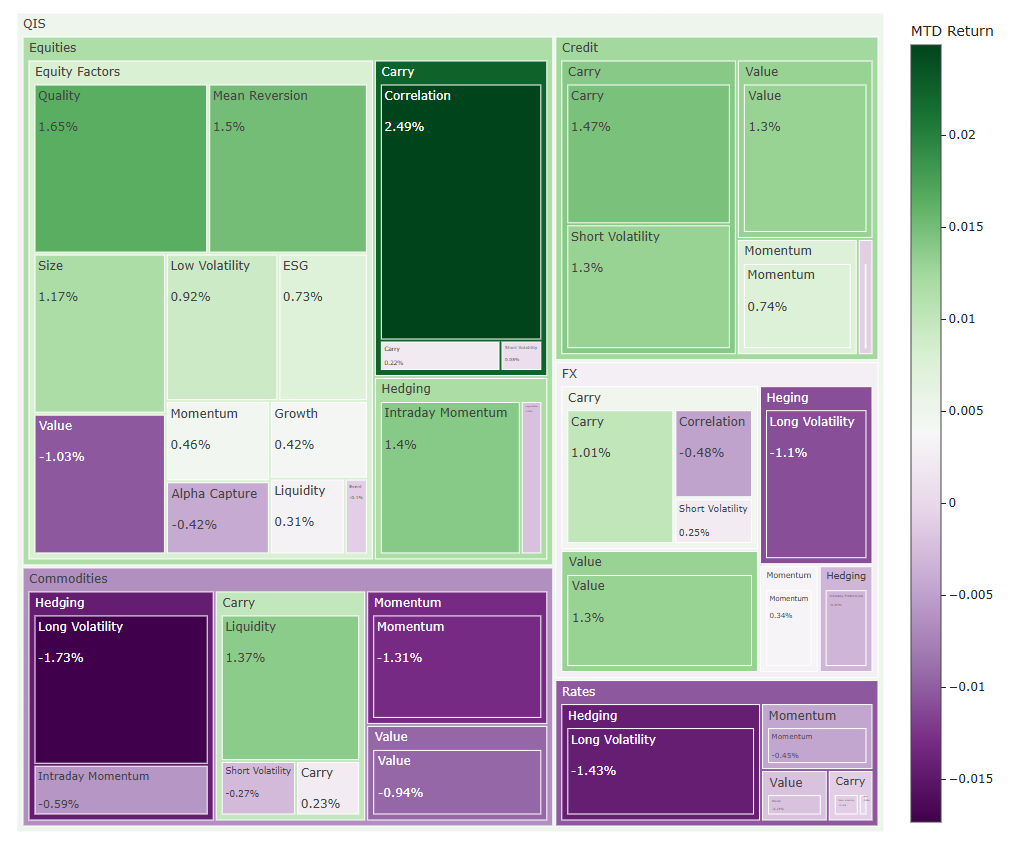

What the numbers said

Average composite return: +0.25%. Median: +0.23%. A little over half of composites finished positive (22 of 40). Those are unremarkable headline numbers — but they sit on top of a very orderly split. What separated the winners from the losers was not the direction of any one market; it was whether a strategy harvests a repricing or gets caught in one.

Dispersion between best and worst was ~4.2 percentage points (best +2.49%, worst –1.73%), in line with May and well short of a crisis regime. Credit was the strongest asset class (+0.94% on average, four of its five composites green); Rates and Commodities were the weakest, both near –0.45%.

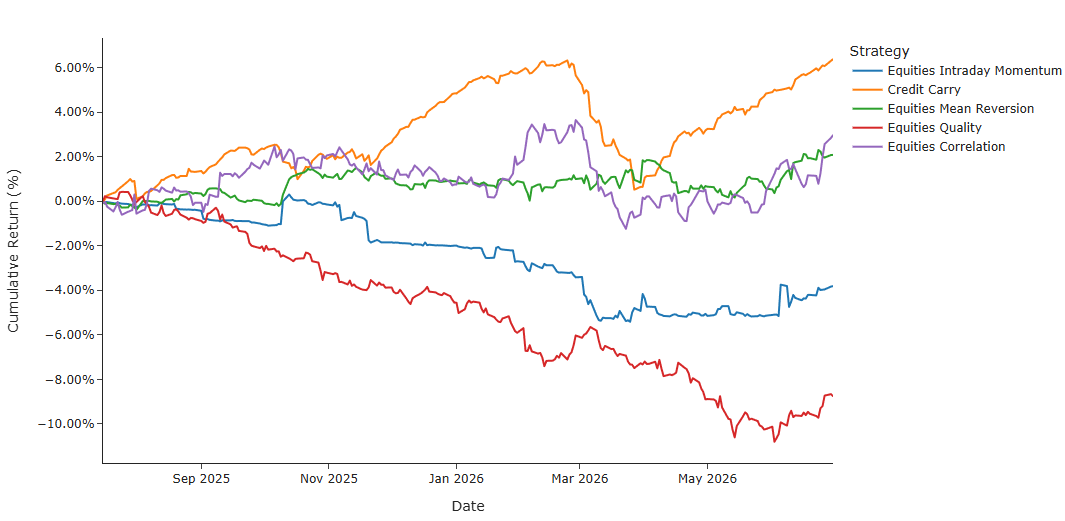

Leaders: Equities Correlation (+2.49%), Equities Quality (+1.65%), Equities Mean Reversion (+1.50%), Credit Carry (+1.47%), Equities Intraday Momentum (+1.40%)

What paid: carry, credit, and the divergence trade

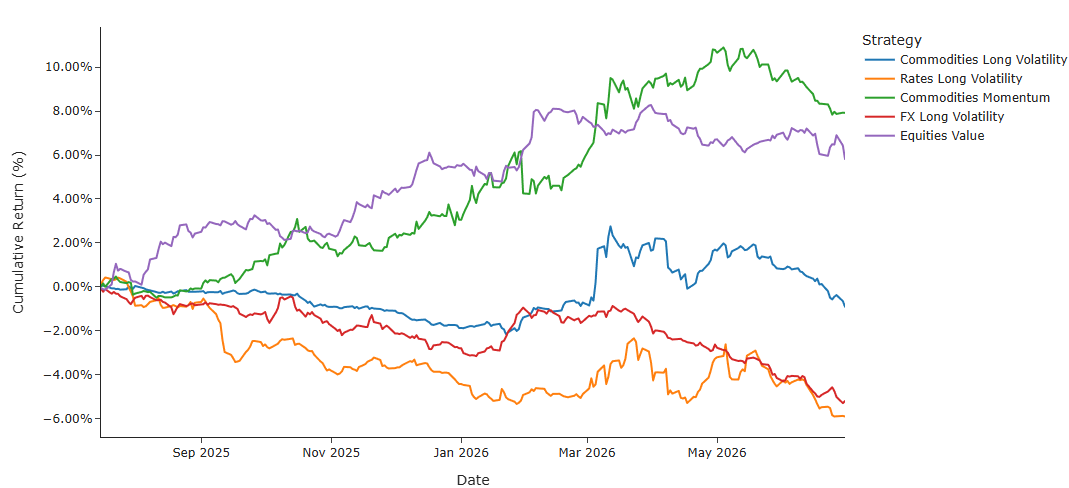

Carry was again the anchor (+0.58% on average, nine of thirteen composites positive), and the standout was credit: four of its five composites finished green, led by Credit Carry (+1.47%) and Credit Short Volatility (+1.30%). Spreads stayed supportive and European sovereign yields eased as cooling inflation pulled some of the hike risk back out of ECB pricing — a textbook backdrop for credit carry to work. Equities Correlation (+2.49%) topped the whole board, the kind of dispersion payoff you get when a market broadens out beneath the index level.

Equity factors were the quiet workhorse, positive as a group (+0.51%, eight of eleven composites up) with a clear defensive tilt on top. Quality (+1.65%) and Low Volatility (+0.92%) — both near the bottom in May — led alongside Mean Reversion (+1.50%), while Value (–1.03%) was the main drag. This was a rotation in emphasis rather than a growth unwind: Growth itself finished modestly positive.

The same dollar strength — a hawkish Fed pivot flagging a possible hike, against a world of central banks mostly on hold — paid the FX value and carry names, with FX Value (+1.30%) and FX Carry (+1.01%) among the month's better composites. The rest of the FX sleeve was mixed, though, so as a bucket it added only modestly (+0.14%).

What paid the bill: trend, convexity, and rates

The other side of the ledger is that path dependency punished everything reversal-sensitive. The oil crash, gold's four-week slide and the round-trip in yields are textbook trend-killers, and Momentum came in negative (–0.17%), with Commodities Momentum (–1.31%) the worst of the group. Hedging was the real drag, though (–0.51%, just one of eight composites positive): the month ended constructively with energy volatility collapsing, so convexity never got paid. Every long-volatility sleeve bled — Commodities (–1.73%), Rates (–1.43%), FX (–1.10%), Equities (–0.21%) and even Credit (–0.10%) — with only choppy-session Equities Intraday Momentum (+1.40%) bucking it. Rates and Commodities were the weakest asset classes, the direct imprint of the hawkish rate repricing and the violent energy reversal.

What we take into July

June reinforces the pattern that has held all year: carry and credit are conditionally powerful, but they are being earned in a market that can reprice the rates and inflation path abruptly. Two swing factors will decide whether the regime holds — whether the Fed's hawkish signal converts into an actual hike, which would keep pressure on rate-sensitive and trend sleeves, and whether the Iran ceasefire holds, since a re-escalation would whipsaw commodities again and finally reward the convexity that has now lagged for two months running.

And that is the uncomfortable part. Two months in a row, the hedges have cost money and the carry has paid. That is precisely the configuration in which protection starts to look expendable — and precisely the configuration in which giving it up is least advisable. The premium you resent paying in a quiet month is the premium you cannot buy in a loud one.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.