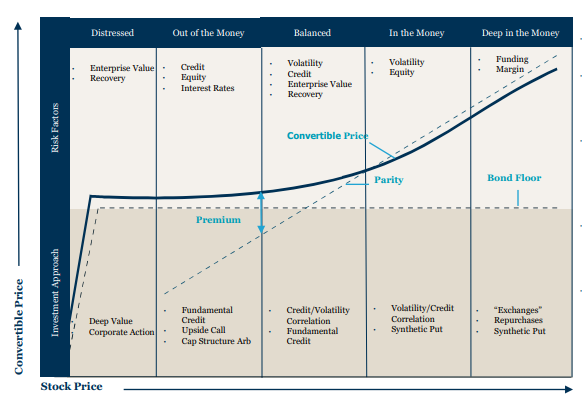

Convertible bonds offer flexibility for investment strategies like outright, arbitrage, volatility-focused, credit-focused, and M&A activity.

2 min read | Sep 7, 2022

Convertible Bonds and convertible arbitrage were high demand Hedge Fund strategies in the 1990’s up through the financial crisis. The confluence of GFC and the subsequent decade plus of QE was devastating for convertible strategies for two reasons.

First, in a systematic credit crisis all bonds are impacted, even convertibles positions significantly hedged with short equity and issued by companies with more cash on their balance sheets than debt. Many a PB took the opportunity to force margin calls on leveraged products and buy themselves money good bonds at thirty to forty cents on the dollar.

In addition, convertible bond issuance plummeted in the subsequent ZIRP decade since issuers could issue straight bonds with low coupons and had no need to give away the equity upside of a convertible bond.

2020 was the first year of significant convertible issuance in a decade. Convertible strategies seem to be steadily returning to relevance as rates and volatility normalize in the post QE era. The reason is the dynamic flexibility of convertible bonds lends itself to a broad spectrum of investment strategies.

Outright: fundamental convertible investment can provide some yield and participation in the equity upside of bull markets. The bond floor insulates the downside exposure in the absence of fraud or significant credit concerns. This asymmetric strategy expresses fundamental equity views with outright long convertibles and some rho hedging.

Arbitrage: Convertible arbitrage strategies can generate returns in a multitude of ways.

-Classic convertible arbitrage goes delta neutral with short stock. The focus here can be fundamental, convexity driven or a blend of both.

-Volatility focused convert arb strategies take advantage of the inherent dampened volatility of the embedded warrants due to the bond floor. Listed options can be sold against the converts for additional yield or to capture convexity This is particularly the case for investment grade bonds approaching an investor put date or maturity. It’s also possible to “Chinese” or short expensive convertible bonds against a long equity hedge.

-Credit focused convert strategies target the frequent mismatch between bonds of different seniority, bonds vs. CDS, converts vs. straights as well as distressed recovery plays.

-In addition, the embedded premium takeout make whole provisions in convertible debt allows investors to profit from or be insulated against M&A activity in their bonds.

-Certain strategies focus on indenture provisions or deal directly with issuer treasury departments exchanging or trading directly with issuers for a profit as the rate environments shift.

In a nutshell, convertibles are a dynamic product with equity,convexity, and credit return drivers. A resurgence in convertible issuance and strategies seems reasonable as volatility and rate environments normalize.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.