Systematic vs discretionary pod platforms: how architecture determines drawdown behaviour, correlation risk, and what allocators are actually underwriting.

8 min read | Apr 5, 2026

The drawdown that rattled markets in March — triggered by a sharp escalation in Middle East tensions and rapid repositioning in energy and rates — did something useful. It separated two structures that are routinely grouped under the same label: multi-strategy hedge funds.

Systematic multi-strategy platforms navigated the episode with relative composure. Several discretionary pod platforms saw sharper, more uneven drawdowns. The performance gap was not about who had the better view on Iran. It was about how each engine is built — and what that means when stress arrives without warning.

This post builds a framework for thinking through that difference. Not to declare a winner, but to understand what you are actually buying when you allocate to either structure.

Two models, one label

The term "multi-strategy" is doing a lot of work in the industry. It describes both a $60bn discretionary platform running 300 independent pods and a systematic macro fund trading 40 signal families across asset classes. The word is accurate for both. It is not particularly useful for either.

The distinction that matters is architectural.

Discretionary pod platforms are, in essence, internal capital allocation businesses. A central firm raises external capital, allocates it across a roster of semi-autonomous portfolio managers, and manages the aggregate risk. Each pod operates with relative independence — its own book, its own process, sometimes its own risk parameters. The firm's job is to hire well, allocate sensibly, and ensure that the aggregate does not blow up when a pod goes wrong.

Systematic multi-strategy funds operate differently. There is no roster of PMs with negotiated mandates. Instead, there is a centrally designed signal library — trend, carry, value, volatility, liquidity, and derivatives strategies — executed through a unified risk and portfolio construction framework. The judgment is embedded in the system design, not in the daily decisions of individual traders.

Both can produce differentiated returns. The risk profiles, however, are structurally distinct.

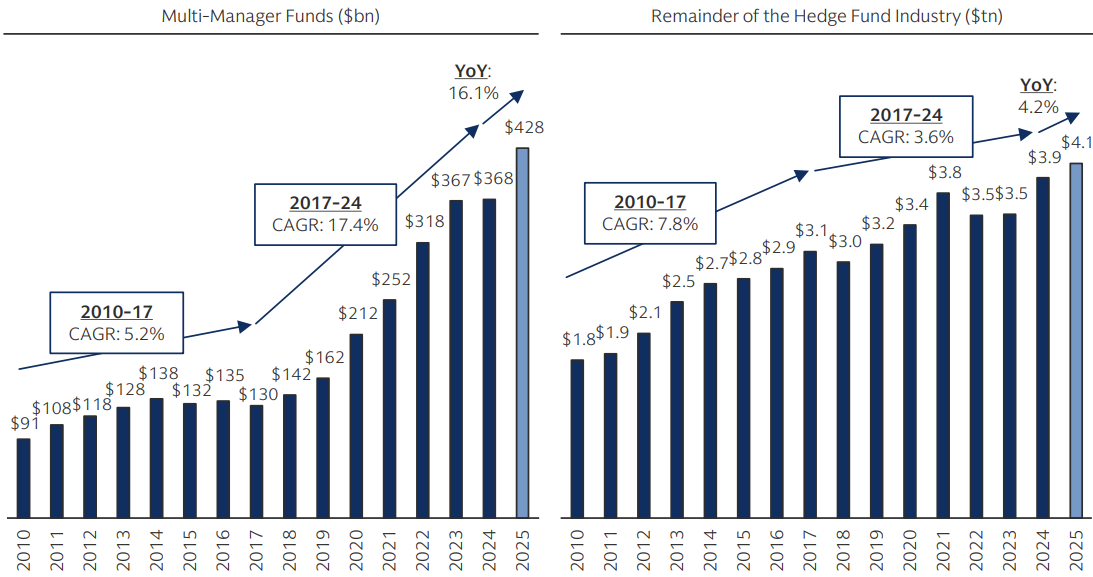

AUM growth in multi-manager funds vs. hedge fund industry, 2010-2025

Source: GS Prime Insights & Analytic; as of end June each year

What drove the March divergence

The Iran event was a fast-moving, geopolitically driven shock — a repricing that happened over days, primarily in energy, Middle East equities, and short-duration rates. Understanding why systematic funds held up better requires looking at each structural layer.

Systematic engines respond to price signals. They do not need a PM to convene, form a view, and decide to act. When energy volatility spiked, trend-following and volatility positioning adjusted automatically, within the logic of their rules. Discretionary pods depend on human reaction speed — which is variable, and which slows further when the event is uncertain and the geopolitical read is contested.

The correlation point is subtler. Discretionary pod platforms are designed to be uncorrelated across PMs at the portfolio level. That assumption holds reasonably well in normal conditions. It holds less well when a macro shock hits multiple pods simultaneously through shared exposures — rates, dollar, energy — that are not always visible at the aggregate level. The March event was precisely this kind of shock: broad enough to clip multiple books at once, fast enough that netting did not absorb the hit.

Systematic multi-strategy funds carry different correlation risk. The strategies are defined by signal type, not by PM discretion, and the correlations across those signals are typically part of the system's explicit design. The risk framework knows, more or less, what moves together — because it was built that way.

On drawdown mechanics, the difference is sequential versus continuous. On discretionary pod platforms, risk management at the aggregate level is largely reactive: the central risk team monitors books, enforces stop-losses, and steps in when a pod breaches limits. The mechanism works, but it follows a sequence — breach, detect, act. On systematic platforms, position sizing and drawdown control are continuous, embedded in the execution logic itself.

None of this means systematic funds are immune to sharp events. They have their own failure modes — overfitting, crowding across trend funds, signal breakdown in regimes the model was not trained on. The March episode simply was not one of those failure modes.

The deeper risk framework

When a professional investor allocates to a multi-strategy structure, three distinct risk layers are in play. Getting clarity on which layer dominates — and who controls it — is more useful than any performance comparison.

Systematic multi-strategy vs. discretionary pod platforms — structural comparison

|

|

Systematic multi-strategy |

Discretionary pod platform |

|---|---|---|

|

How it works |

Signal library — trend, carry, value, volatility, derivatives |

Human judgment — semi-autonomous PMs with individual mandates |

|

Transparency |

Model risk — signal decay, regime change, systematic crowding | Talent risk — PM attrition, hidden correlation, aggregate book opacity |

|

Operational complexity |

Continuous Embedded in execution logic; real-time position sizing |

Sequential Central risk team monitors and intervenes: breach → detect → act |

|

LP auditability |

Explicitly modelled — signal correlations designed into the system | Assumed low across pods; can spike in macro shocks via shared exposures |

|

Common geography |

Higher Logic is documented; risk attribution is systematic |

Lower Returns depend on discretionary judgment; harder to attribute ex ante |

|

Due diligence burden |

Model and signal review; regime testing; crowding analysis |

PM-by-PM assessment; aggregate book transparency; talent pipeline |

|

Best suited for |

Portfolios prioritizing process consistency, drawdown discipline, and risk transparency | Portfolios targeting non-replicable alpha where the DD capability exists |

Source: Resonanz Capital.

Strategy risk is the risk that the underlying trading strategies stop working. For systematic funds, this is model risk — the signals are no longer predictive, or the edge has been arbitraged away. For discretionary platforms, this is talent risk — the PMs lose their edge, burn out, or leave.

Aggregation risk is the risk that diversification at the portfolio level breaks down. On pod platforms, this shows up as correlation among pods in stressed markets. On systematic platforms, it shows up as strategy crowding — when too many systematic funds hold similar positions and a forced unwind cascades.

Operational and structural risk is the risk embedded in the vehicle itself — counterparty exposure, fee structures, liquidity terms, leverage management, and the durability of the risk management infrastructure. This layer is often the least visible and the most consequential in a tail event.

The March episode was primarily an aggregation risk event. It showed up differently across the two architectures, and the systematic structure managed it better in this specific instance.

What each architecture actually offers

Systematic multi-strategy earns its place in allocations where consistency of process, drawdown discipline, and transparency of risk attribution matter most. It is well-suited to environments where correlation management at the portfolio level is the core objective. The risk budget is explicit, behaviour under different market regimes can be modelled, and the logic is documented rather than discretionary — which matters when the allocation needs to be defended in front of an investment committee.

Discretionary pod platforms earn their place where the primary objective is exposure to genuine alpha generation from skilled PMs — returns that are not systematically replicable and that depend on the quality of specific human judgment. The best pod platforms produce returns that systematic engines cannot. The trade-off is that correlation management is more opaque, drawdown behaviour in tail scenarios is less predictable, and the due diligence burden is substantially higher.

The allocation question, properly framed, is not which is better. It is: what am I underwriting, and do I have the process to underwrite it well?

What March confirmed, not what it resolved

The March event confirmed something experienced alternatives investors already knew: architecture is not a secondary consideration. It is the investment. The strategy mix, the risk management infrastructure, the correlation assumptions, the response speed — these are the product. Performance attribution flows from these structural choices.

What March did not resolve is the longer-term question. Systematic multi-strategy has real vulnerabilities in regime change — a sharp shift in factor correlations, a breakdown in trend signal quality, or a crowding event in the systematic space can produce its own sharp drawdown. Discretionary pod platforms, when the pods are genuinely skilled and the risk management is sophisticated, can produce return streams that no model will replicate.

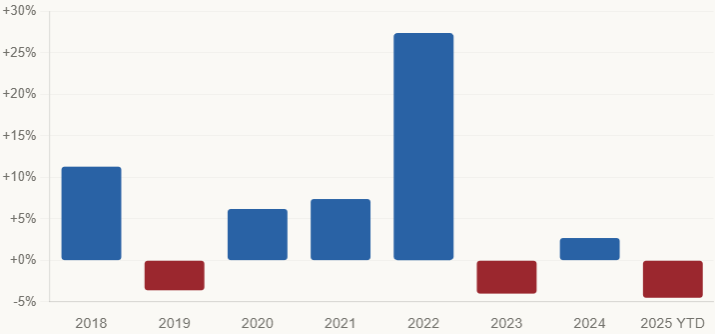

SG CTA Trend Index — annual returns (%)

Source: Société Générale Prime Services · Illustrates regime dependency of systematic trend strategies

You are not choosing between a good structure and a bad one. You are choosing between two different engines, each with a defined failure mode, each earning its place under different conditions. Knowing which failure mode you can most afford — and which you can most effectively monitor — is where the allocation decision actually lives.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.