How allocators should size macro: define the job, separate strategy types, and build a sleeve that actually changes portfolio outcomes.

14 min read | Mar 16, 2026

A 1% macro allocation cannot hedge a portfolio. It can decorate one.

Yet that is approximately where most institutional macro sleeves sit — large enough to appear on the asset allocation chart, too small to change outcomes in the scenarios they were funded to address. In a 30% equity drawdown, a 1% managed futures sleeve generating 25% returns contributes less than one percentage point of offset to the total fund. That is not a hedge. That is a rounding error with a good story attached.

The sizing problem is a symptom of a deeper one: most allocators have not defined what the sleeve is actually there to do. Macro is not one thing. Discretionary global macro, systematic macro, and managed futures solve different problems, behave differently across regimes, and fail differently when the environment turns against them. Treating them as interchangeable — or buying a token allocation to "something different" — is how institutions end up with a sleeve that is expensive, disappointing, or both.

The right question is not whether you believe in macro. The right question is: what job do you want the sleeve to do, and how large does it need to be for that job to show up at the total-portfolio level?

Step One: Define the Job

The sleeve can serve three distinct roles. Most allocators conflate them.

The shock absorber is the clearest job. Here, the allocator wants gains — or at minimum, non-correlation — during sustained equity or bond stress. Managed futures and trend-following CTAs are the cleanest fit. They can go long or short liquid futures across rates, currencies, commodities, and equity indices, and they have historically delivered their strongest returns in the deep, sustained dislocations that damage the rest of a portfolio most. In 2008, trend-following strategies broadly delivered strong positive returns as equity markets fell more than 40%. In 2022, when both equities and bonds fell simultaneously and broke the 60/40 diversification logic, managed futures again delivered meaningfully positive returns. Those are the environments the strategy is built for.

Source: Return Stacked Portfolio Solutions; underlying data from AQR, Société Générale CTA Trend Index, Robert Shiller data, and Yahoo Finance. Monthly returns use AQR “A Century of Trend Following Investing” (Jan. 1, 1940–Dec. 31, 1999) and Société Générale CTA Trend Index (Jan. 1, 2000–Mar. 31, 2025). Pre-2000 trend data are simulated/hypothetical and scaled to match the arithmetic average monthly return and standard deviation of the live Société Générale CTA Trend Index. S&P 500 TR uses Yahoo Finance ^SP500TR extended with Robert Shiller’s S&P 500 data.

The regime diversifier is the classic role for discretionary global macro and broader systematic macro. The sleeve is expected to express views on rates, curves, FX, inflation, and policy divergence. It is not pure crisis insurance — it is a diversifier that can make money when the dominant market narrative changes, whether that means an inflation regime, a growth slowdown, or a policy divergence between central banks. The risk is that a discretionary macro manager with a large rates book overlaps significantly with fixed income exposures already held elsewhere in the portfolio. Diversification that duplicates existing bets is not diversification.

Macro returns across monetary policy regimes

Source: Graham Capital, HFR, Inc., Federal Reserve of St. Louis, December 2024. The outperformance (annualized) of macro hedge fund strategies is represented by the HFRI Macro (Total) Index.

Source: Graham Capital, HFR, Inc., Federal Reserve of St. Louis, December 2024. The outperformance (annualized) of macro hedge fund strategies is represented by the HFRI Macro (Total) Index.

The return-seeking diversifier is the weakest use case and the one most likely to produce disappointment. If macro is being funded simply as "something different," with no explicit expectation for crisis behavior or regime response, it tends to be undersized, mis-benchmarked, and the first line item cut when the committee loses patience. If you cannot articulate what problem the sleeve solves, it probably doesn't solve one.

That distinction matters because each flavor of macro behaves differently — and fails differently.

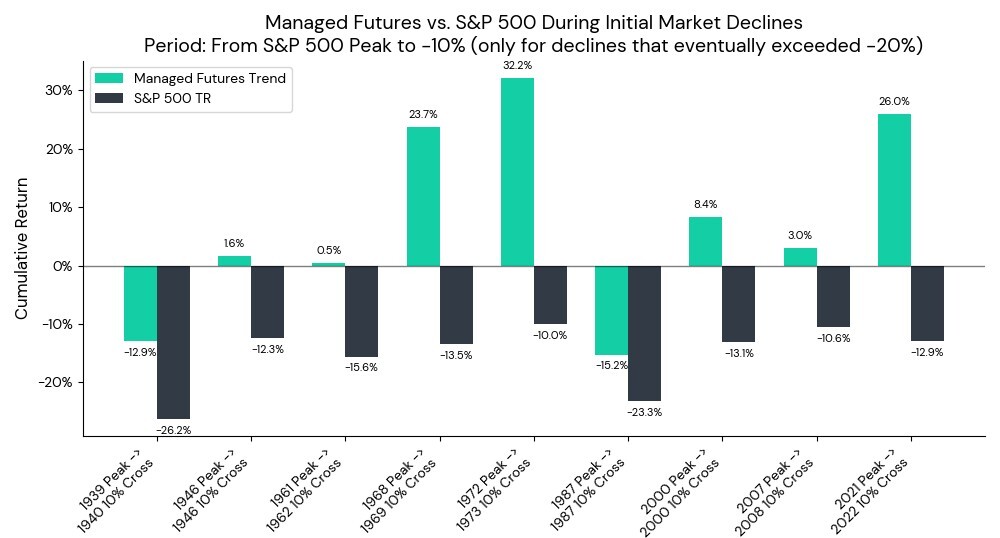

Crisis Alpha Is Real. It Is Also Narrower Than Marketing Decks Suggest.

The managed futures literature is specific about when these strategies tend to help.

AlphaSimplex's work on trend following and crisis alpha makes the point precisely: looking at S&P 500 drawdowns greater than 5%, short-term drawdowns were difficult for trend-following strategies, while deeper and longer drawdowns were the environment in which trend-following was much more likely to deliver positive returns.

Trend-Following’s ‘Crisis Alpha’ Credentials

Source: Man Group, BarclayHedge, Bloomberg; Between 1 January 1987 and 31 March 2023.

Source: Man Group, BarclayHedge, Bloomberg; Between 1 January 1987 and 31 March 2023.

That is the point most allocators miss. A 10% equity correction that reverses in six weeks is not the environment managed futures are built for. A sustained 30–40% drawdown driven by a genuine regime shift — a global financial crisis, a sustained inflation shock, a multi-year bear market — is exactly the environment they are built for. The strategy works by capturing persistent trends across multiple asset classes simultaneously. Short, sharp reversals create whipsaw losses. Sustained directional moves create sustained profits.

The implication is uncomfortable but important: if your committee will judge the macro sleeve on whether it made money in every 8% equity wobble, the strategy will always disappoint. It is not designed to pass that test, and no amount of manager selection will change that. The patience premium is structural, not a manager-specific failure.

Academic evidence is consistent with this. Research on CTAs confirms they provide diversification benefits during crises, while emphasizing that the source of crisis alpha depends on the nature of the crisis itself — specifically whether it is the kind that produces sustained, tradeable trends across liquid futures markets.

Performance of SG Trend Index program during corrections and crisis

Source: The Hedge Fund Journal, Quantica

Source: The Hedge Fund Journal, Quantica

Even within trend-following, manager dispersion is large. Société Générale's industry data has shown that pairwise correlation among SG Trend constituents can be high — around 0.78 in recent periods — while the range of returns across those same managers spans nearly 15 percentage points. High correlation does not mean identical outcomes. Manager construction still matters, even within a strategy that is supposed to be systematic.

How to Size It: The Math That Most Allocators Skip

Start with the job. Then size the sleeve to the portfolio effect you want — not to a neat round number or a peer comparison.

Here is the arithmetic that should drive the decision.

Assume a portfolio that is 60% equity, 30% bonds, 10% other. In a 30% equity drawdown with bonds roughly flat — consistent with what happened in 2022 when inflation broke the equity-bond correlation — the portfolio loses approximately 18% at the total-fund level.

For a macro sleeve to contribute a visible offset — say 3 to 4 percentage points of protection — it needs to be sized at roughly 10 to 15% of the portfolio and generate returns in the range of 25 to 30% in that scenario. That is consistent with what well-constructed managed futures programs delivered in both 2008 and 2022.

A 3% sleeve generating the same 25 to 30% contributes less than 1 percentage point of offset. The committee notices a 3-point improvement in a bad year. They do not notice a 0.75-point improvement. The first is a hedge. The second is a rounding error.

That arithmetic has three direct implications.

First, if the job is shock absorption, the minimum effective size is probably in the 8 to 15% range for most institutional portfolios, depending on the volatility of the macro strategy and the equity weight of the rest of the portfolio. A 2 to 3% sleeve is optics, not insurance.

Second, if budget constraints force a smaller allocation, the job needs to be redefined. A 3% sleeve can contribute to regime diversification and improve the portfolio's return path across growth and inflation regimes without needing to deliver crisis alpha at scale. That is a legitimate role — but it is a different role, with a different benchmark and a different patience budget.

Third, the sizing decision and the role definition cannot be made independently. If the committee agrees the sleeve is a shock absorber but approves a 2% allocation, there is a governance problem that no manager selection process will fix.

The three-step practical framework:

Step one: Define the benchmark for the sleeve. A crisis hedge should not be benchmarked to cash plus 300 basis points. It should be judged on portfolio payoff in stress scenarios — specifically whether it contributed the offset it was sized to provide. A regime diversifier can be assessed on excess return over cash and its contribution to portfolio Sharpe across different regimes. The benchmark should follow the job, not the other way around.

Step two: Size against scenarios. Run the portfolio through at least three historical shocks: a deep equity drawdown like 2008, an inflation shock like 2022, and a bond selloff with equity resilience like 2013's taper tantrum. Ask what contribution the macro sleeve needs to make in each scenario to justify its place, and back-solve the sizing from there. If the required contribution implies a return that the strategy cannot realistically deliver, either the sizing needs to increase or the role needs to change.

Step three: Stress the governance, not just the portfolio. If the sleeve underperforms for 18 months — which is well within the normal experience of trend-following strategies in choppy, trendless markets — will the committee hold it? If the honest answer is no, the allocation is too large for the institution's patience budget, or the role has not been explained clearly enough to the committee. Governance failure is the most common reason macro sleeves are cut at exactly the wrong moment.

The Five Mistakes Allocators Make

Under-sizing. The sleeve is too small to matter, so it delivers frustration rather than diversification. This is the most common mistake and the one most easily diagnosed: if the sleeve cannot move total-fund outcomes in the scenario it was funded to address, it is too small.

Buying the wrong flavor. A discretionary macro manager is hired to provide crisis convexity, or a trend program is hired to express a house view on central bank policy. Those are different mandates. Discretionary macro can express central bank views but is exposed to timing risk and PM judgment in ways that systematic trend is not. Trend-following provides crisis convexity only in the right kind of crisis — one that produces sustained, directional moves, not violent reversals.

Double-counting diversification. An institution that already owns real assets, inflation-linked bonds, and a large rates book may believe it is adding diversification when it buys a discretionary macro manager with a large rates and commodities book. Run the overlap before sizing. The diversification benefit may be much smaller than the allocation implies.

Benchmarking badly. Managed futures are often judged against equities in quiet years and fired just before the regime they are built for finally arrives. The 2010 to 2019 period — a decade of suppressed volatility, compressed trends, and relentlessly rising equity markets — was the worst possible environment for trend-following. Many allocators fired their CTA programs in 2019 or 2020, just before 2022 delivered exactly the sustained, directional moves the strategy is designed to capture. The benchmark should define what success looks like before the period of underperformance begins, not after.

Ignoring manager dispersion. High pairwise correlation among trend managers does not mean identical outcomes. A 15-percentage-point spread in annual returns among managers following the same broad strategy is not noise. Manager construction — signal mix, speed, market breadth, sizing methodology — produces meaningfully different outcomes, particularly in transition periods between trend regimes.

| Macro approach | Primary return engine | Best portfolio role | When it tends to help | What can go wrong | Allocator watchpoint |

|---|---|---|---|---|---|

| Discretionary global macro | PM judgment on rates, FX, curves, policy divergence | Regime diversifier | Policy shifts, cross-market dislocations, big macro narratives | Wrong thesis, concentration, overlap with existing rates/inflation bets | Scenario overlap with rest of portfolio |

| Systematic macro | Rules-based signals across liquid macro markets | Diversifier with cleaner process control | Persistent moves across rates/FX/equity indices | Model crowding, signal decay, whipsaws | Signal horizon, turnover, risk controls |

| Managed futures / CTA trend | Time-series momentum in futures | Shock hedge / crisis alpha sleeve | Deep, sustained drawdowns and multi-asset trends | Short, sharp reversals; “CTA winter” when trends break abruptly | Role clarity and patience budget |

| Short-term traders | Very short holding periods, tactical dislocations | Tactical diversifier | Brief macro dislocations, event-driven volatility | Less crisis convexity than medium-term trend | Do not confuse with strategic hedge |

What to Monitor — And What Specifically to Watch For

Liquidity fit: Check the gap between the fund's stated redemption terms and the actual position-level liquidity in the book. A managed futures fund offering monthly liquidity while holding positions that take 30 or more days to unwind without market impact has a structural mismatch that will surface at the worst moment. The signal is not the redemption terms themselves — it is the time-to-unwind for the 10 largest positions under a stress scenario.

Overlap with existing exposures: Run a quarterly factor regression of the macro sleeve's returns against the portfolio's existing rates duration, inflation sensitivity, and equity beta. If the R-squared is drifting upward over time, the sleeve is becoming more redundant — you are paying for diversification you are not getting. The signal is correlation drift, not a one-time check at the point of allocation.

Strategy style drift: Watch whether the manager's holding period, position concentration, or market breadth has changed materially from the mandate you underwrote. A trend program that has shortened its average holding period to capture more short-term signals is a different product from what you bought. A discretionary macro manager who has quietly built a large equity long book is taking on beta that was not in the original mandate.

Governance patience: Track the committee's actual behavior in prior dry periods — how quickly questions arose, whether informal pressure to reduce the allocation built before a formal review, whether the benchmark shifted post-hoc to make recent underperformance look worse. Historical committee behavior predicts future behavior more reliably than stated conviction. If the committee became impatient after 12 months of flat returns in the last cycle, plan accordingly — either by sizing the allocation down to a level the committee can genuinely hold, or by investing in the education required to extend the patience budget.

Allocator Takeaways

Define the job before sizing. Shock absorber, regime diversifier, and return-seeking macro are different mandates with different benchmarks, different sizing requirements, and different patience budgets. A sleeve that serves all three jobs simultaneously serves none of them well.

Size to impact, not to optics. Run the arithmetic. If the sleeve cannot contribute a visible offset in the scenario it was funded to address, it is too small to be a hedge. Resize it or redefine its role — but do not maintain a token allocation and call it risk management.

Benchmark by function, not by convention. A crisis hedge should be judged on portfolio payoff in stress. A regime diversifier should be judged on its contribution to portfolio Sharpe across regimes. Cash-plus benchmarks applied to shock-absorption mandates will always produce the wrong conclusion at the wrong moment.

Stress the governance, not just the portfolio. The most common cause of macro sleeve failure is not strategy underperformance — it is committee impatience at exactly the point in the cycle when the strategy is most likely to pay off next. Size to the institution's actual patience budget, and define success criteria before the dry period begins.

Macro belongs in institutional portfolios. The mistake is not owning it. The mistake is owning it without deciding what it is there to do — and without sizing it to actually do it.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.