March 2026 saw increased volatility and a focus on trend and convexity, as energy shocks reshaped risk assets and highlighted the limits of carry strategies.

5 min read | Apr 5, 2026

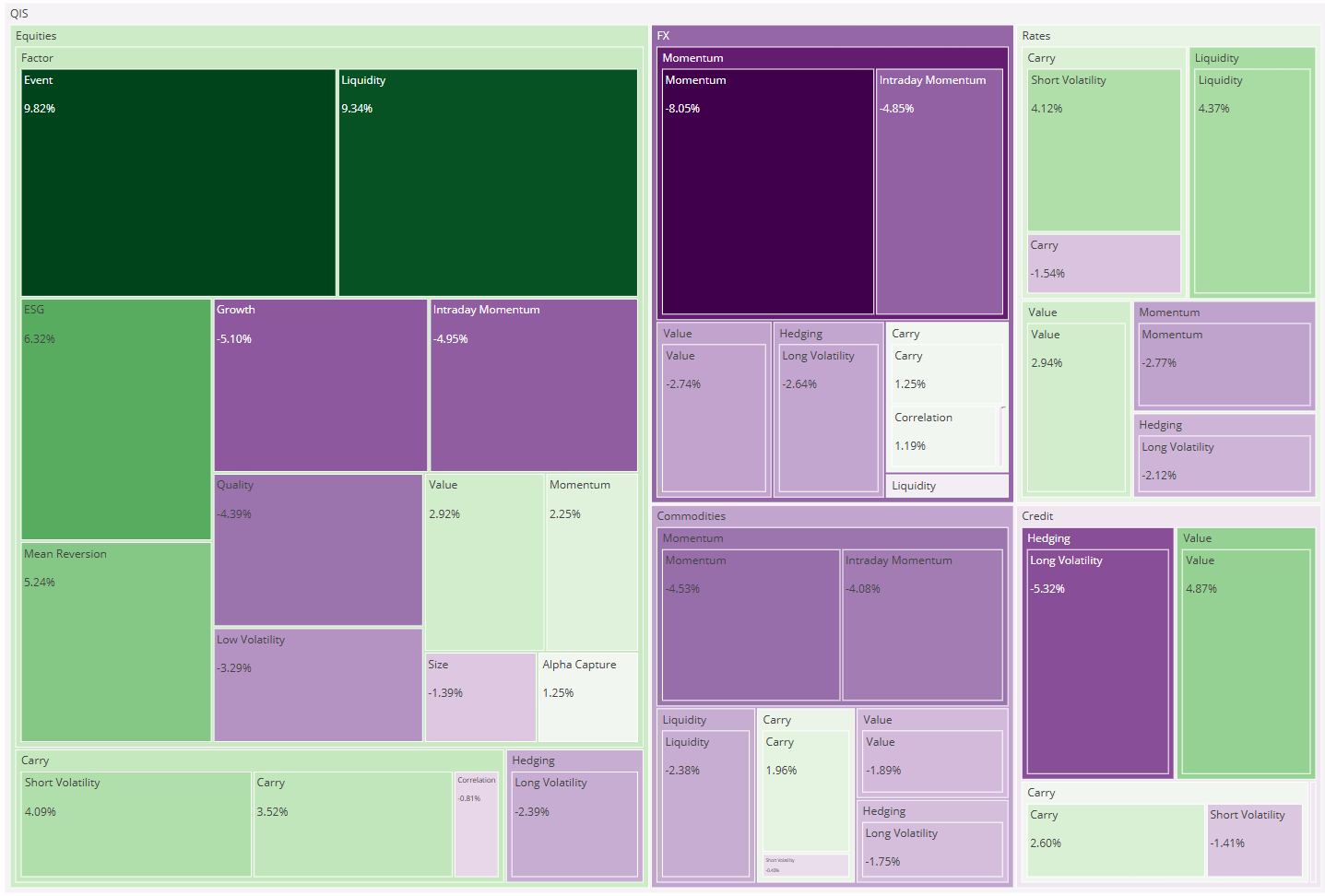

March delivered a classic energy-shock regime: sharp moves in oil and rates dominated cross-asset behavior, and QIS outcomes largely followed the playbook—trend and convexity held up, while carry, liquidity, and credit risk premia struggled.

- Average QIS composite return: –1.25% MTD.

- Breadth: only 30% of composites finished positive (12 out of 40).

- Dispersion: ~9.4 percentage points between the best and worst composites (+2.59% vs –6.81%).

- What worked: Commodities Momentum (+2.59%), Commodities Long Volatility (+2.42%), Rates Long Volatility (+1.72%), Equities Mean Reversion (+0.88%), FX Carry (+0.85%).

- What didn’t: Commodities Carry (–6.81%), Commodities Liquidity (–5.80%), Credit Carry (–4.66%), Credit Value (–4.52%), Equities Growth (–3.15%).

Market backdrop

March was dominated by a geopolitical-driven energy shock that quickly became the primary macro variable for risk assets. Disruption risk around energy shipping routes pushed crude sharply higher and repeatedly forced markets to toggle between risk-off and headline-driven relief rallies.

The move in oil translated into renewed inflation anxiety and a repricing in rates: U.S. yields rose meaningfully through the month (with the 10-year peaking above 4.4% late-month before easing to ~4.3% at month-end). Equity markets broadly sold off across regions despite a strong final-day bounce—consistent with an environment where the “duration” of the shock mattered more than growth optimism. Credit spreads widened, but remained far from crisis levels—more indicative of macro uncertainty than systemic stress.

This backdrop is important for QIS because it tends to:

- Punish carry when curves reprice quickly and financing/roll assumptions break down,

- Reward momentum and long volatility when directional moves and vol-of-vol rise,

- Create equity factor dispersion (energy sensitivity, pricing power, and “real economy” exposures matter more than classic growth narratives).

QIS performance in March

The key message from the QIS cross-section is that March was less about “beta up/down” and more about which exposures you were paid to hold.

- Convexity was valuable. The strongest composites were those designed to benefit from trend persistence or volatility expansion—particularly in commodities and rates.

- Carry became asymmetric. In fast repricings—especially those driven by supply shocks—carry strategies can shift from steady income to sudden drawdown behavior.

- Credit was a weak link. Even with “only” moderate spread widening, the combination of higher yields and risk premia repricing created a tough environment for systematic credit exposures.

Top-five performers (MTD)

- Commodities Momentum: +2.59% — Benefited from the persistent directional impulse in energy and related spillovers.

- Commodities Long Volatility: +2.42% — A strong month for commodity convexity as price and volatility dynamics became more discontinuous.

- Rates Long Volatility: +1.72% — Helped by the rate back-up and higher uncertainty around inflation expectations and central bank reaction functions.

- Equities Mean Reversion: +0.88% — Consistent with a month that featured sharp selloffs punctuated by fast relief rallies.

- FX Carry: +0.85% — Held up better than typical “pure risk-off” episodes, suggesting carry dynamics remained supported despite higher macro noise.

Bottom-five performers (MTD)

- Commodities Carry: –6.81% — The defining casualty of the month; rapid curve and front-end repricing dominated carry assumptions.

- Commodities Liquidity: –5.80% — A month where liquidity conditions and execution frictions mattered; energy shocks tend to stress microstructure and depth.

- Credit Carry: –4.66% — Hit by higher yields and wider spreads; carry became vulnerable in a regime shift.

- Credit Value: –4.52% — Reflects repricing in credit risk premia as macro uncertainty rose.

- Equities Growth: –3.15% — Long-duration growth struggled in a month where inflation risk and rates sensitivity reasserted themselves.

Average performance by group

- Hedging: –0.41% (avg.)

- The “right” type of hedging helped (notably long vol in rates/commodities), but this was partially offset by losses in more tactical/short-horizon signals and weaker credit-hedging performance.

- Momentum: –0.49% (avg.)

- Commodities momentum was the standout positive, but momentum exposures in other asset classes faced a more complex tape (rates/FX/credit had more reversals and less clean persistence).

- Equity Factors: –0.81% (avg.)

- A split month: mean reversion, value, and size provided support, while growth and several “quality/defensive” style exposures lagged—consistent with an environment where energy sensitivity and rate exposure drove relative performance.

- Value: –1.76% (avg.)

- The bucket was dragged by rates value and credit value, even as FX value was mildly supportive—highlighting that “value” behaves very differently across asset classes under an inflation/energy shock.

- Carry: –2.20% (avg.)

- The weakest bucket overall, dominated by the drawdowns in commodity carry/liquidity and broad weakness in credit carry. A few offsets (e.g., FX carry, select equity premia) were not enough to change the picture.

Quarter-end snapshot (YTD through March 2026)

The quarter-to-date picture is already shaped by a small number of dominant themes:

- Average composite YTD: –0.84%, with ~43% of composites positive.

- Leadership has been commodity-dominated, with commodities trend/convexity among the strongest year-to-date.

- The largest drag remains commodity carry, reinforcing how quickly carry can become path-dependent when macro regimes shift.

Conclusion

March reinforced a core lesson for systematic allocation: supply shocks compress the value of “steady premia” and increase the value of convexity. In practical terms:

- Carry can look attractive—until the regime changes and curve dynamics overwhelm the roll-down thesis.

- Rates are not guaranteed to hedge equities when the shock is inflationary or energy-driven.

- Diversification across trend, volatility, and carefully sized carry exposures remains the most robust design principle when macro outcomes are headline-dependent.

If the energy shock persists into April, dispersion should remain elevated—rewarding strategies that can adapt to rapid regime changes while keeping carry exposures appropriately constrained.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.