April 2026 saw a market rebound driven by earnings resilience and the AI capex cycle, highlighting the strength of carry strategies amid geopolitical stress.

3 min read | May 5, 2026

The defining dynamic in April's QIS tape was not the market rally — it was what the rally revealed about return premia structure. Carry came back broadly. Convex hedges gave back, as they should in a genuine risk-on month. And FX once again demonstrated why it remains the most regime-sensitive sleeve in any multi-strategy portfolio.

The Market Setup That Mattered

Despite ongoing Middle East tensions, the market rotated firmly toward earnings resilience and the AI capex cycle. The detail that explains QIS outcomes is not the equity rally itself — it is the credit/duration split beneath it. Sovereign duration remained impaired by energy-driven inflation. Credit spreads tightened and carry held up. That distinction shows up directly in the strategy-level returns.

What the Tape Said

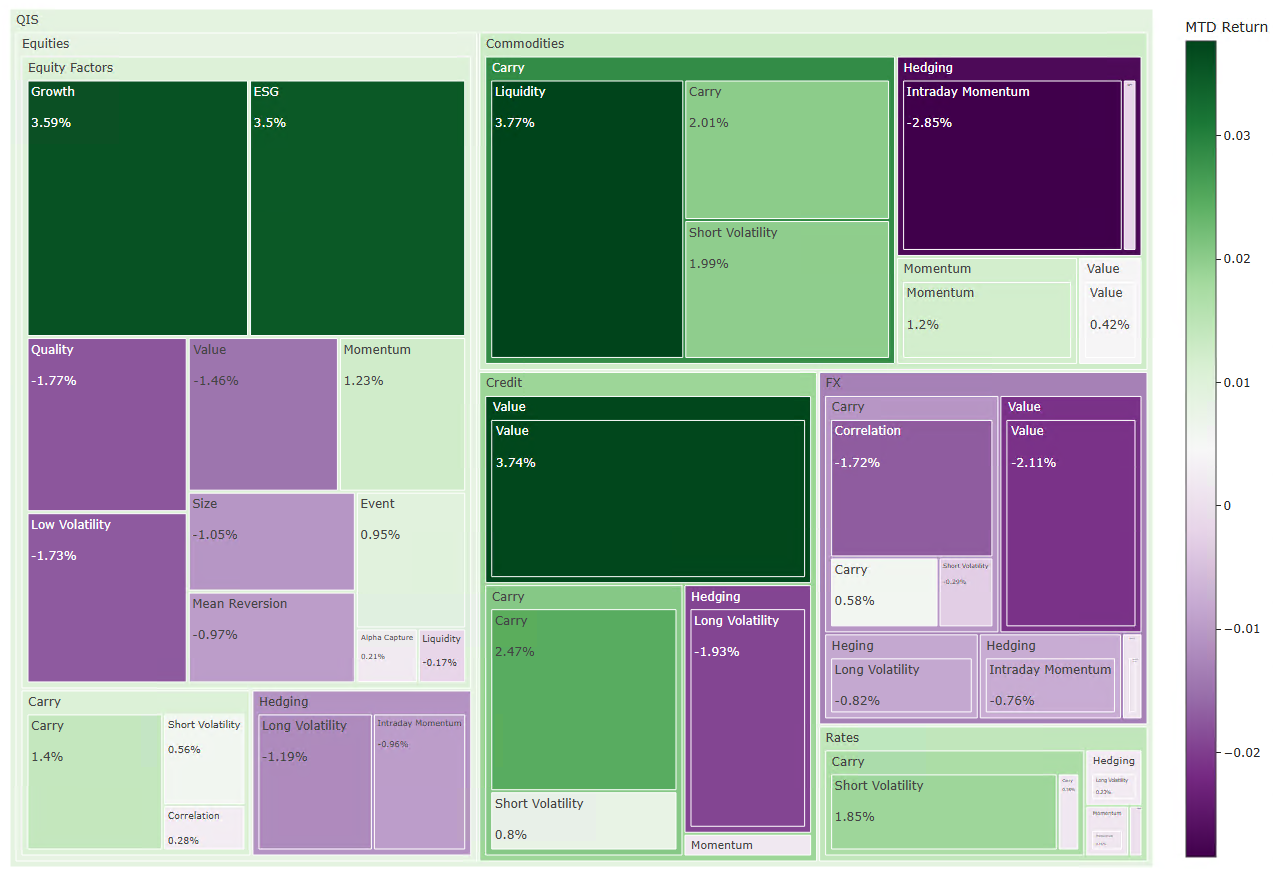

MTD summary: Average composite +0.29% (median +0.18%) · 60% of composites positive · Dispersion ~6.6pp (best +3.77%, worst –2.85%) · Carry led (+1.07% avg.) · Hedging lagged (–1.06% avg.)

Carry delivered with breadth, not just magnitude — credit carry, credit value, and commodity liquidity premia all contributed, reflecting genuine risk appetite recovery across multiple premia simultaneously.

Equity factors averaged +0.21%, but the internal story matters more: Growth and ESG captured the AI/earnings upside; Quality and Low Volatility lagged sharply. The market was paying for participation, not protection.

Hedging lost –1.06% on average. That is the correct outcome in a strong rebound month — the issue is not that hedges lost, but whether March's gains were preserved at the portfolio level. One tension worth tracking: the speed of the March-to-April regime flip raises questions about regime-detection architecture, not just hedge sizing.

FX averaged –0.72%. Value and correlation strategies struggled against directional, policy-sensitive moves — including a sharp late-month JPY move consistent with intervention. FX remains the sleeve most vulnerable to event risk overwhelming mean-reversion frameworks.

Top and Bottom Performers

Top five: Commodities Liquidity +3.77% · Credit Value +3.74% · Equities Growth +3.59% · Equities ESG +3.50% · Credit Carry +2.47%

Bottom five: Commodities Intraday Momentum –2.85% · FX Value –2.11% · Credit Long Volatility –1.93% · Equities Quality –1.77% · Equities Low Volatility –1.73%

Dispersion of 6.6pp on a +0.29% average month reinforces the point: strategy selection and sizing continue to matter more than beta exposure.

YTD and the Road Into May

The average composite remains –0.44% YTD — a useful reminder that concentrated premia exposure means a single shock month (March) can dominate the early-year scorecard in a way broad market beta rarely does.

Heading into May, the key risk is straightforward: if energy keeps sovereign volatility elevated, carry stays conditional, duration hedging stays impaired, and FX sensitivity remains elevated. The QIS premia landscape is functioning as designed. What it requires is calibrated sizing — not structural change, but clear-eyed acknowledgment that the macro environment is conditionally supportive, not unconditionally so.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.