A plain-English guide to the Treasury basis trade: cash–futures spread, repo leverage, margin risk, and the weekly indicators allocators should monitor.

8 min read | Feb 23, 2026

In April 2020, the Federal Reserve injected $1.6 trillion into Treasury markets in a matter of weeks. The proximate cause wasn't a credit crisis or a bank run. It was a leveraged carry trade unwinding faster than the plumbing could handle.

That trade was the Treasury basis trade. It's back. It's bigger. And most allocators are still underwriting it like a spread product.

This guide is for the allocator who doesn't need to become a rates trader, but does need to understand why this trade fails — and what to watch before it does.

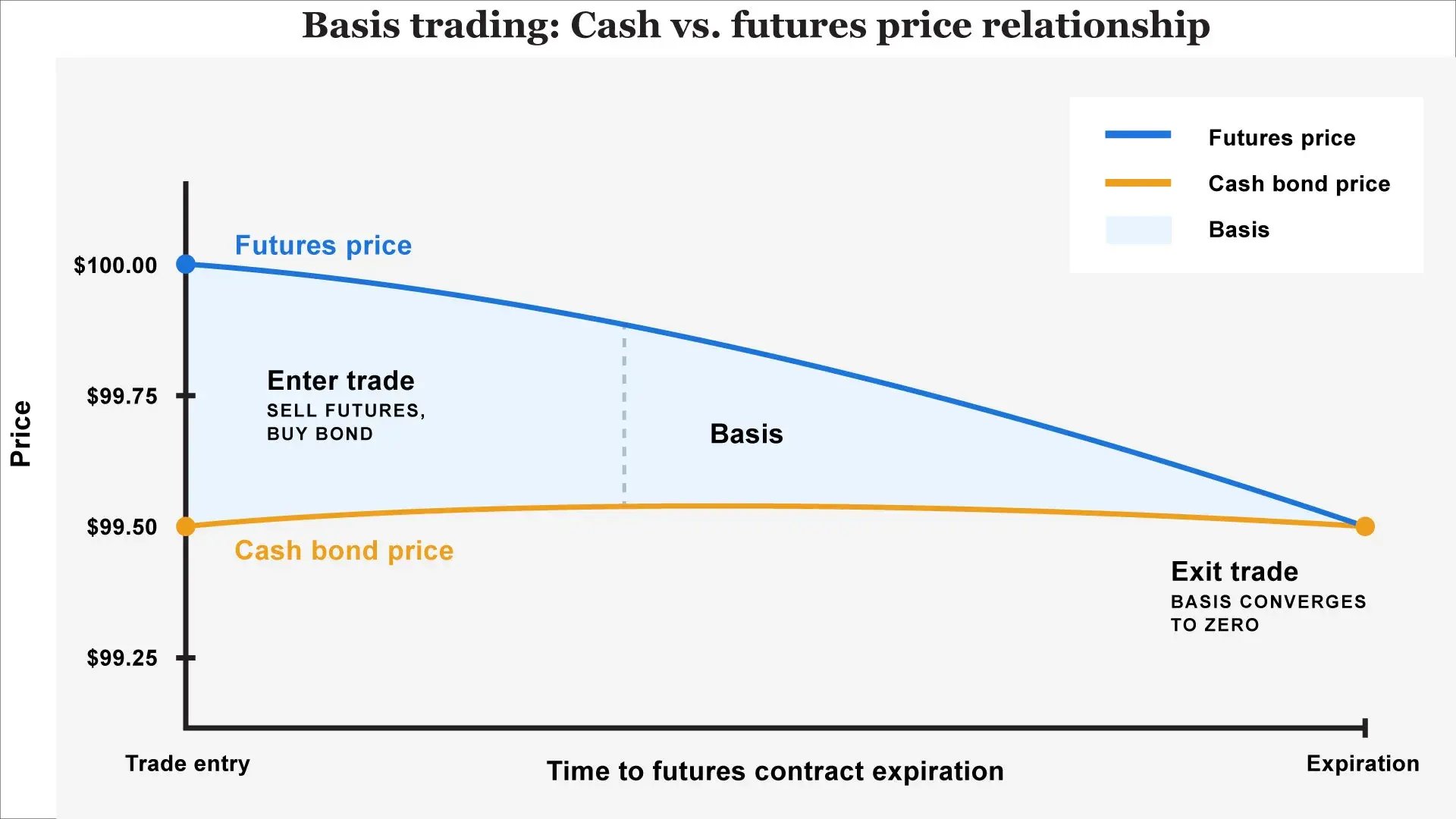

What the Trade Is, in Plain English

For a given Treasury maturity, you can trade in two closely related markets: cash Treasuries (the actual bonds) and Treasury futures (exchange-traded contracts referencing deliverable Treasuries).

In theory, the futures price should reflect the cash bond price, plus or minus the cost of financing the bond in repo, adjusted for delivery economics. When the relationship deviates, a "basis" opens. Hedge funds and relative-value desks try to capture it.

The mechanics are straightforward: buy the cash Treasury, finance it in repo, short the futures contract against it, and earn the net spread. If that spread is small — say a few basis points annualized — the only way to make it matter is leverage.

And leverage is where the story really begins.

Source: Britannica, Inc

Why It Looks "Low Risk" Until It Isn't

Leverage is structural, not optional

The bond is financed in repo. Haircuts on Treasuries are often low — sometimes effectively near zero for certain counterparties. That makes the trade capital-light until haircuts rise or funding becomes scarce.

The OFR's NCCBR dataset work shows that a large share of repo outstanding can carry zero haircuts, with Treasuries dominating that bucket. That does not mean infinite leverage. It means the system is acutely vulnerable to a sudden change in terms.

Share of Outstanding Repo by Haircut Type (percent)

Haircut Distribution by Counterparty Type (percent share)

Source: OFR Non-Centrally Cleared Repo Collection, Authors’ analysis.

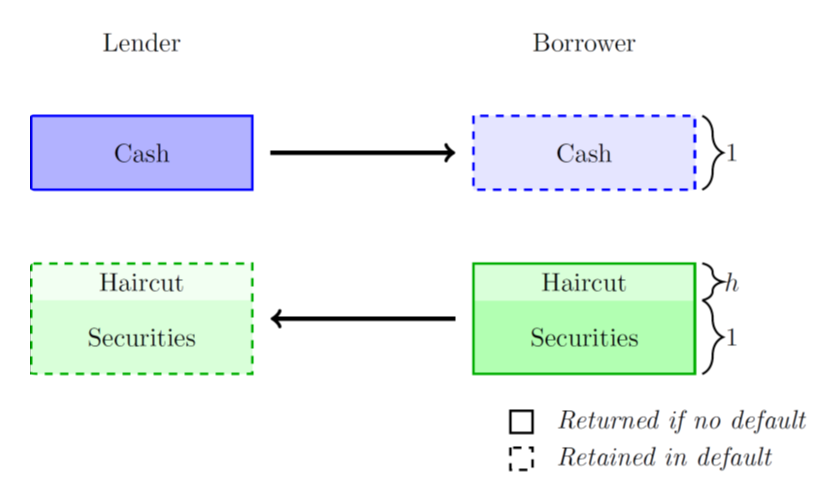

Two margin regimes — and they move against you simultaneously

This is the key insight: a basis book has two separate collateral requirements that can both tighten at the worst moment.

Repo haircuts, set by dealers, rise when balance sheets are constrained or counterparty risk increases. Futures margin, set by clearing houses, rises when volatility rises. When markets get jumpy — exactly when you'd want to hold the trade — both move against you at once. The fund needs more cash at precisely the moment cash is most expensive.

Haircuts and margining in a typical repo transaction

Source: OFR Non-Centrally Cleared Repo Collection, Authors’ analysis

Dealer balance sheet is the gating factor

Even if the basis represents genuine arbitrage, it must be intermediated through dealer balance sheets. When dealers pull back — at quarter-end, under regulatory pressure, during volatility events — the basis can widen further, funding reprices, and an orderly unwind becomes a disorderly one.

The Four Ways It Blows Up

Failure Mode A: Repo tightens → forced deleveraging

When repo rates spike or dealers reduce availability, the fund needs more cash to maintain the same bond position. If it can't post additional collateral, it sells bonds. Selling bonds into a stressed market widens the basis further. The cycle feeds itself.

Allocator framing: this is liquidity risk, not spread risk.

Failure Mode B: Futures margin jumps → variation margin drain

Rates volatility spikes. Futures move sharply. Margin requirements rise. Cash is pulled from the fund to meet margin calls — even if the trade is theoretically hedged over time. Timing matters. The fund can be right about the ultimate convergence and still face a margin call it can't meet today.

Allocator framing: basis funds can be market-neutral and still fail due to cashflow timing.

Failure Mode C: Basis widens before it converges

Mark-to-market losses from a widening basis prompt risk managers and counterparties to tighten terms, forcing the unwind that causes further widening. This is not a theoretical sequence. It is what happened in March 2020, and why Fed intervention was required to contain spillovers.

Failure Mode D: The exit is crowded

The basis trade is structurally concentrated: it targets the most liquid government bond market in the world using common instruments, with participants who share similar risk limits. When those limits hit across a large cohort simultaneously, correlated selling overwhelms the market's capacity to absorb it.

.webp?width=1600&height=900&name=Basis-Trade-instructional-chart%20(2).webp)

Source: Britannica, Inc

Underwriting It Like an Allocator

You'll encounter this trade inside relative value / fixed income arbitrage funds, macro RV pods, multi-strat pods, and occasionally "low volatility income" wrappers — the last of which should be an immediate red flag. The underwriting posture should be the same in all cases: this is a leveraged financing trade, not a spread product.

The Questions That Actually Differentiate

On financing:

- Which repo venues — bilateral, tri-party, or cleared? Bilateral is the least transparent and where terms can change fastest.

- What are haircuts today, and what's the fund's policy when a dealer unilaterally raises them? A fund that says "our dealers have never changed terms on us" hasn't been through a stress event.

- How concentrated is counterparty exposure? Three prime brokers is not diversification.

On liquidity buffers:

- What percentage of NAV is held in unencumbered cash or near-cash, available immediately for margin calls?

- How long does it take to reduce the book by 30% without moving the market? Get a specific number, not a range.

- What are the internal de-risk triggers, and who has authority to pull them?

On risk measurement:

- Do they model delivery optionality — specifically CTD switches under stress?

- What does the basis look like in their worst-case scenario, and does that scenario exceed March 2020?

- How are they sizing for margin calls that happen simultaneously across repo and futures?

On leverage and concentration:

- Give us leverage ranges, not point estimates. If the answer is a single number, push harder.

- What's the concentration by tenor? A 10-year-heavy book has different liquidity characteristics than one spread across the curve.

- What's the worst-case funding assumption embedded in their stress test?

On dealer dependency:

- What fraction of financing runs through the top two counterparties?

- What happens to the book at quarter-end when dealers reduce balance sheet availability?

- Has the fund ever been told a repo line was being reduced? How did they respond?

What to Watch Weekly

Monitor the plumbing, not the narrative. A basis trade that looks fine in a quarterly letter can be under severe stress in the daily funding markets.

Repo stress signals: SOFR spikes relative to administered rates are where tightness shows up first. SRF (Standing Repo Facility) usage is a secondary signal — elevated usage means private repo is strained enough that counterparties are going to the Fed instead.

Volatility and margin regime: Sharp rates moves that increase futures margin requirements are the trigger for Failure Mode B. Track not just the level of volatility but the direction of travel — a rapid rise in rates vol over two to three days is when margin calls cluster.

Dealer intermediation capacity: Widening bid-ask spreads and reduced depth in on-the-run Treasuries are a leading indicator that dealers are pulling back. Quarter-end stress is predictable; watch for it specifically in late March, June, September, and December.

| What to monitor (weekly) | Where it shows up | Why it matters for basis risk | “Bad” direction |

|---|---|---|---|

| SOFR and repo rate spikes | FRED/NY Fed | Signals funding tightness and rollover risk | Higher / more volatile |

| SRF usage | Fed/NY Fed reporting (news) | Private repo strain; backstop being tapped | Rising usage |

| Haircut behavior (where observable) | OFR NCCBR insights | Higher haircuts = forced deleveraging pressure | Haircuts rising |

| Rates volatility regime | Vol indices / market moves | Higher vol increases futures margin and VAR limits | Volatility rising |

| Clearing reform milestones | SEC releases | Shifts margining, balance sheet usage, and plumbing | Implementation risk during transition |

| Dealer intermediation capacity | Bid-ask/depth, commentary | Dealers are the gate; pullback widens basis | Liquidity thinning |

The Bottom Line

The Treasury basis trade is not free carry. It is leveraged financing plus margin mechanics wrapped around a small spread. The dominant risk is forced selling when repo terms tighten or futures margin rises — and those two things tend to happen at the same time, during the same events, for the same reasons.

The funds that survive stress events are not necessarily the ones with the best trade construction. They're the ones with the most conservative financing terms, the deepest liquidity buffers, and the clearest de-risk triggers. That's what you're underwriting.

Size RV Treasury exposure like a liquidity-sensitive trade. Because that's what it is.

Resonanz insights in your inbox...

Get the research behind strategies most professional allocators trust, but almost no-one explains.